Best High-Yield Savings Accounts for 2026: Earning Over 5.0% APY

Anúncios

Latest developments on Best High-Yield Savings Accounts for 2026: Earning Over 5.0% APY on Your Deposits, with key facts, verified sources and what readers need to monitor next in Estados Unidos, presented clearly in Inglês (Estados Unidos) (en-US).

Best High-Yield Savings Accounts for 2026: Earning Over 5.0% APY on Your Deposits is shaping today’s agenda with new details released by officials and industry sources. This update prioritizes what changed, why it matters and what to watch next, in a straightforward news format.

The Evolving Landscape of High-Yield Savings in 2026

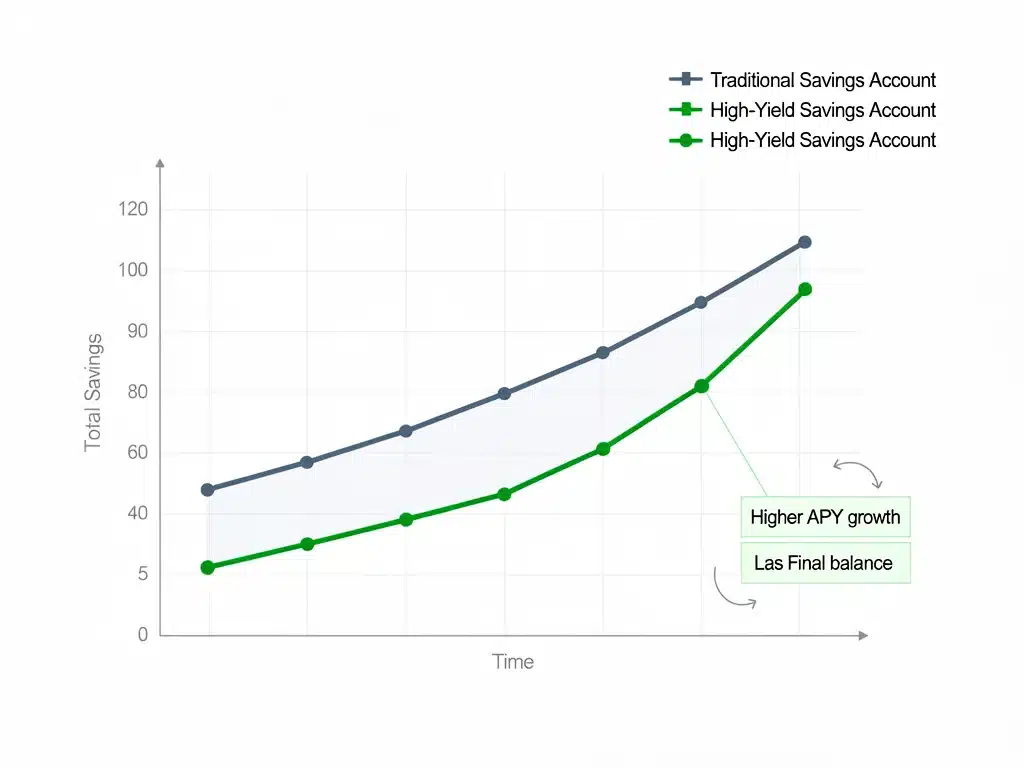

The financial sector is currently experiencing dynamic shifts, with interest rates remaining a focal point for savers. Projections for 2026 indicate a robust environment where high-yield savings 2026 accounts are poised to offer competitive APYs, potentially exceeding the 5.0% mark.

Anúncios

This favorable outlook stems from a combination of economic factors, including central bank policies and market demand for stable deposit options. Consumers in the United States are increasingly seeking avenues to maximize their idle cash, making high-yield savings accounts a compelling choice.

Understanding these trends is crucial for anyone looking to optimize their financial strategy and ensure their money works harder for them. The emphasis on high-yield savings 2026 reflects a broader move towards more financially savvy decisions among the populace.

Key Factors Driving High APY Offers

Several economic indicators and banking strategies are converging to create an environment conducive to higher APYs. The Federal Reserve’s stance on interest rates, inflation management, and the competitive nature of the digital banking space all play significant roles.

As the economy continues to stabilize and grow, banks are looking to attract and retain deposits, often by offering more attractive rates. This competition directly benefits consumers seeking the best high-yield savings 2026 options.

Moreover, the operational efficiencies of online-only banks allow them to pass on greater savings to their customers in the form of higher annual percentage yields. This structural advantage often positions them as leaders in the high-yield savings account market.

Understanding Inflation and Interest Rates

Inflation directly impacts the real return on your savings, making high interest rates even more critical. When inflation is high, your purchasing power erodes, so an APY above the inflation rate is essential to truly grow your wealth.

The Federal Reserve’s adjustments to the federal funds rate serve as a benchmark for interest rates across the banking industry. Historically, periods of higher federal funds rates correlate with increased APYs on savings accounts, including those for high-yield savings 2026.

The Role of Digital Banks

Digital banks operate with significantly lower overhead costs compared to traditional brick-and-mortar institutions. This operational efficiency allows them to offer more competitive interest rates to attract a larger customer base.

- Lower operating expenses translate directly into higher APYs for customers.

- Accessibility and convenience through online platforms appeal to a broad demographic.

- Innovative features and user-friendly interfaces enhance the overall banking experience.

Identifying Top High-Yield Savings Accounts for 2026

As 2026 approaches, several institutions are expected to lead the charge in offering competitive high-yield savings accounts. These often include online-only banks, credit unions, and some challenger banks that prioritize customer deposits.

Prospective savers should look beyond just the APY and consider factors such as FDIC insurance, minimum balance requirements, and any potential fees. A holistic approach ensures that the chosen account truly meets individual financial needs for high-yield savings 2026.

Researching customer reviews and financial health ratings of these institutions can also provide valuable insights into their reliability and service quality. This due diligence is paramount when selecting the best high-yield savings 2026 option.

Key Features to Look For

Beyond the impressive APY, several features define a truly superior high-yield savings account. These include easy access to funds, robust online platforms, and excellent customer service.

- FDIC Insurance: Ensures your deposits are protected up to $250,000 per depositor, per institution.

- No Monthly Fees: Avoids erosion of your earnings through unnecessary charges.

- Low or No Minimum Balance: Allows flexibility for all types of savers to benefit from high-yield savings 2026.

- Easy Transfers: Seamless integration with external accounts for convenient money movement.

Comparing Leading Institutions

When evaluating potential providers for high-yield savings 2026, a direct comparison of their offerings is essential. Focus on their advertised APYs, any introductory bonuses, and their long-term rate stability.

Some banks might offer slightly lower APYs but compensate with superior mobile banking experiences or integrated financial planning tools. The best choice often balances high returns with practical usability for high-yield savings 2026.

Maximizing Your Earnings with High-Yield Savings

Simply opening a high-yield savings account is the first step; actively managing it can significantly boost your overall returns. This involves understanding how interest is calculated, setting up automated transfers, and regularly reviewing market rates.

Taking advantage of compound interest is a powerful strategy, where your interest earnings also begin to earn interest over time. The longer your money stays in a high-yield savings 2026 account, the more substantial this effect becomes.

Establishing clear financial goals, such as saving for a down payment or an emergency fund, can also motivate consistent contributions to your high-yield savings 2026 account. This disciplined approach is key to long-term financial success.

The Power of Compound Interest

Compound interest is often referred to as the eighth wonder of the world due to its exponential growth potential. It means that the interest you earn is added to your principal, and then that new, larger principal earns interest.

Over time, even a small difference in APY can lead to a significant difference in total earnings, especially with high-yield savings 2026. Starting early and contributing regularly amplifies this effect, making your money work harder for you.

Automating Your Savings

Setting up automatic transfers from your checking account to your high-yield savings account is a simple yet effective way to ensure consistent savings. This removes the need for manual intervention and reduces the temptation to spend the money.

Many banks offer customizable transfer schedules, allowing you to align contributions with your paydays. This hands-off approach makes building your savings effortless and consistent, crucial for high-yield savings 2026.

Understanding the Risks and Safeguards

While high-yield savings accounts are generally considered low-risk, it’s important to be aware of potential fluctuations in interest rates and to ensure your funds are protected. The primary safeguard for depositors in the US is FDIC insurance.

Interest rates are subject to market conditions and central bank policies, meaning they can change over time. While high-yield savings 2026 projections are positive, monitoring these trends is always a wise practice.

Choosing an FDIC-insured institution mitigates the risk of losing your deposits in the unlikely event of a bank failure. This fundamental protection provides peace of mind for savers utilizing high-yield savings 2026 accounts.

FDIC Insurance Explained

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects depositors against the loss of their insured deposits if an FDIC-insured bank or savings association fails. This protection is standard for most reputable high-yield savings 2026 accounts.

Each depositor is insured up to at least $250,000 per insured bank, per ownership category. Understanding these limits is crucial, especially if you have significant savings across multiple accounts or institutions.

Monitoring Rate Changes

Interest rates on high-yield savings accounts are variable, meaning they can change at any time based on market conditions. Regularly checking the APY offered by your bank and competitors is a good habit.

If your bank significantly drops its rates, it might be time to consider transferring your funds to another institution offering a more competitive APY for high-yield savings 2026. This proactive approach ensures you’re always earning the most.

Comparing High-Yield Savings with Other Investment Options

While high-yield savings accounts offer attractive returns and low risk, it’s beneficial to understand how they stack up against other investment vehicles. Options like Certificates of Deposit (CDs), money market accounts, and even short-term bonds have different risk-reward profiles.

High-yield savings accounts typically offer more liquidity than CDs, allowing easier access to your funds without penalty. This flexibility is a significant advantage for emergency funds or short-term savings goals, especially with high-yield savings 2026.

For long-term growth and higher potential returns, diversified investment portfolios might be more suitable, but they come with increased risk. High-yield savings 2026 accounts serve as a foundational component of a balanced financial plan.

High-Yield Savings vs. CDs

Certificates of Deposit (CDs) generally offer fixed interest rates for a specified term, providing predictable returns. However, they typically penalize early withdrawals, limiting liquidity.

- CDs offer fixed rates, providing certainty over a set period.

- High-yield savings accounts offer variable rates but greater flexibility.

- Choosing depends on your need for liquidity versus rate certainty for high-yield savings 2026.

High-Yield Savings vs. Money Market Accounts

Money market accounts (MMAs) often blend features of checking and savings accounts, offering competitive interest rates and check-writing privileges. However, their APYs might not always match the highest-yield savings accounts.

MMAs typically have higher minimum balance requirements than many high-yield savings accounts. For savers prioritizing liquidity and minimal balance restrictions, high-yield savings 2026 often presents a more straightforward option.

Strategic Planning for Your Savings Goals

Effective financial planning involves aligning your savings strategy with your short-term and long-term goals. High-yield savings accounts are particularly well-suited for specific objectives, such as building an emergency fund, saving for a down payment, or accumulating funds for a major purchase.

By categorizing your savings and allocating them to appropriate accounts, you can optimize both growth and accessibility. The stability and competitive returns of high-yield savings 2026 make it an ideal choice for these crucial financial milestones.

Regularly reviewing your financial plan and adjusting your savings contributions ensures you stay on track toward achieving your objectives. This proactive approach is vital for leveraging the benefits of high-yield savings 2026.

Building an Emergency Fund

An emergency fund is a critical component of financial security, providing a buffer against unexpected expenses. Placing this fund in a high-yield savings account ensures both safety and growth.

The liquidity offered by high-yield savings accounts means your emergency funds are readily accessible when needed, without penalties. This combination of safety, accessibility, and competitive APY makes high-yield savings 2026 ideal for this purpose.

Saving for Major Purchases

Whether it’s a new car, a home down payment, or a significant vacation, high-yield savings accounts can accelerate your progress toward these goals. The higher APY helps your money grow faster than in a traditional account.

Setting specific targets and timelines for these purchases can help you determine how much to contribute regularly to your high-yield savings 2026 account. This structured approach fosters discipline and brings your goals closer within reach.

The Future Outlook for High-Yield Savings in the US

The trajectory for high-yield savings accounts in the United States remains positive, with experts predicting continued strong performance into 2026 and beyond. Economic stability and ongoing competition among financial institutions will likely sustain attractive APYs.

Technological advancements in banking are also expected to further enhance the user experience and accessibility of these accounts. This continuous innovation benefits consumers looking for efficient and rewarding savings solutions, including high-yield savings 2026.

Staying informed about market developments and regulatory changes will be key for savers to continuously adapt their strategies and capitalize on the best available high-yield savings 2026 opportunities. The financial landscape is ever-changing, and vigilance pays off.

Technological Innovations in Banking

The rise of fintech has revolutionized how consumers interact with their money, making banking more convenient and efficient. Mobile apps, AI-powered financial insights, and seamless digital platforms are now standard offerings.

These innovations not only improve the customer experience but also contribute to the operational efficiency of banks, enabling them to offer higher APYs on high-yield savings 2026. The future promises even more integrated and personalized banking solutions.

Regulatory Environment and Consumer Protection

Regulatory bodies continue to play a crucial role in ensuring the safety and soundness of the financial system, which directly impacts high-yield savings accounts. Consumer protection measures are also evolving to safeguard depositors.

Changes in banking regulations can influence how banks operate and the rates they offer. Keeping an eye on these developments ensures that your high-yield savings 2026 choices remain secure and compliant with current standards.

| Key Point | Brief Description |

|---|---|

| High APY Outlook | Projections for 2026 show high-yield savings accounts exceeding 5.0% APY due to economic factors. |

| Digital Bank Advantage | Online-only banks offer superior rates due to lower operational costs and increased competition. |

| FDIC Protection | Deposits are insured up to $250,000, ensuring safety and peace of mind for savers. |

| Maximizing Returns | Utilize compound interest and automated transfers to significantly boost savings growth. |

Frequently Asked Questions About High-Yield Savings Accounts

High-yield savings accounts typically offer significantly higher interest rates (APYs) compared to traditional savings accounts. This difference stems from lower overhead costs of online banks and increased competition, allowing your money to grow much faster over time. They often come with fewer physical branches but robust online services.

Yes, reputable high-yield savings accounts are just as safe as traditional ones, provided they are offered by FDIC-insured institutions. The Federal Deposit Insurance Corporation (FDIC) protects your deposits up to $250,000 per depositor, per institution, in case of a bank failure. Always verify FDIC insurance before depositing funds.

Beyond the Annual Percentage Yield (APY), consider factors like minimum balance requirements, monthly fees, ease of transferring funds, and customer service quality. Also, check if the account is FDIC-insured and read recent customer reviews to gauge overall satisfaction and reliability for your high-yield savings 2026 needs.

To maximize earnings, take advantage of compound interest by leaving your money untouched for longer periods. Set up automated transfers to consistently contribute to your account, and regularly monitor market rates. If another institution offers a significantly higher APY, consider moving your funds to optimize your high-yield savings 2026.

While projections for high-yield savings 2026 are optimistic, interest rates are variable and subject to economic conditions and central bank policies. Experts anticipate competitive rates to persist, but it’s crucial to stay informed about market trends. Regular monitoring ensures you adapt your strategy to always secure the best possible returns.

Looking Ahead: Sustaining Growth with High-Yield Savings

The current financial climate presents a unique opportunity for savers to significantly grow their wealth through high-yield savings 2026 accounts. The expectation of APYs exceeding 5.0% underscores a competitive banking environment driven by economic factors and digital innovation.

As we move towards 2026, the emphasis will continue to be on informed decision-making, ensuring that consumers select accounts that offer both high returns and robust security. Leveraging these accounts strategically can be a cornerstone of a resilient personal finance plan.

Staying vigilant about market changes and regulatory updates will empower individuals to continuously optimize their savings strategies, making the most of the promising landscape for high-yield savings 2026. This proactive approach is essential for long-term financial health.