Maximizing Your 2026 Roth IRA Contributions: Hit the $7,000 Limit

For individuals aiming for Maximizing Your 2026 Roth IRA Contributions: Strategies to Hit the $7,000 Limit, understanding the latest financial regulations is crucial. This guide provides essential strategies and verified insights to optimize your retirement savings, focusing on eligibility and effective contribution methods.

Recent financial updates and expert analyses highlight key opportunities for increasing your Roth IRA contributions. We delve into practical steps and considerations for navigating income limits and maximizing tax-advantaged growth.

This article offers a direct, objective overview of how to effectively manage your 2026 Roth IRA contributions. It ensures you are equipped with the knowledge to make informed decisions for a secure financial future.

Anúncios

Maximizing Your 2026 Roth IRA Contributions: Strategies to Hit the $7,000 Limit is a critical financial goal for many looking to secure their retirement. With the potential for tax-free growth and withdrawals in retirement, the Roth IRA remains an indispensable tool for long-term financial planning.

Understanding the contribution limits, income thresholds, and available strategies is paramount to fully leveraging this powerful retirement vehicle. This article delves into the specifics of the 2026 Roth IRA landscape, providing actionable insights to help you reach the maximum contribution.

We will explore the eligibility requirements, discuss the nuances of the $7,000 limit, and outline advanced strategies like the backdoor Roth IRA, ensuring you are well-informed to optimize your retirement savings.

Understanding the 2026 Roth IRA Contribution Limit

The Internal Revenue Service (IRS) periodically adjusts contribution limits for various retirement accounts, including the Roth IRA. For 2026, the projected individual contribution limit for a Roth IRA is set at $7,000.

Anúncios

This limit applies to individuals under age 50; those aged 50 and older are typically eligible for an additional catch-up contribution, further increasing their savings potential. Staying informed about these adjustments is crucial for effective financial planning.

These limits are designed to encourage retirement savings while also reflecting economic conditions and inflation. Understanding how these figures are determined provides valuable context for your long-term financial strategy.

What the $7,000 Limit Means for You

The $7,000 limit represents the maximum amount an eligible individual can contribute to their Roth IRA in 2026. This contribution can be made in a lump sum or through regular payroll deductions throughout the year.

It is important to note that this limit is per individual, not per household. Therefore, if both spouses are eligible, they can each contribute up to $7,000 to their respective Roth IRAs.

Adhering to this limit is essential, as over-contributing can lead to penalties and administrative complexities. Careful tracking of your contributions is a key part of Maximizing Your 2026 Roth IRA Contributions.

Eligibility Requirements for Direct Contributions

Direct contributions to a Roth IRA are subject to Modified Adjusted Gross Income (MAGI) limits, which typically vary based on filing status. For 2026, these income thresholds will be updated by the IRS.

If your MAGI exceeds these limits, your ability to contribute directly to a Roth IRA may be phased out or eliminated entirely. It is crucial to verify the exact income limits for 2026 as they become available from the IRS.

Understanding these income limitations is the first step in determining your direct contribution eligibility and whether alternative strategies are necessary for Maximizing Your 2026 Roth IRA Contributions.

Navigating Income Thresholds and Phase-Out Rules

Roth IRA eligibility is not universal; it is primarily determined by your income level. The IRS establishes specific Modified Adjusted Gross Income (MAGI) thresholds that dictate whether you can contribute directly, contribute a reduced amount, or are entirely phased out.

For 2026, while the exact income limits are yet to be officially released, historical trends suggest a continued upward adjustment. It is imperative to consult official IRS guidelines or a financial advisor as these figures become available to ensure compliance.

These phase-out rules are designed to target the tax benefits of Roth IRAs towards middle-income earners, but strategies exist for higher-income individuals to still participate.

Understanding the MAGI Limits for 2026

The MAGI thresholds for 2026 will determine if your income allows for direct Roth IRA contributions. For single filers, there will be a lower threshold where full contributions are permitted, and an upper threshold where contributions are completely disallowed.

For those filing as married filing jointly, the income limits are generally higher. If your income falls within the phase-out range, your maximum contribution amount will be proportionally reduced.

Tracking your MAGI accurately is vital for Maximizing Your 2026 Roth IRA Contributions, as miscalculations can lead to penalties. Consulting a tax professional can help clarify your specific situation.

Strategies for High-Income Earners

For individuals whose income exceeds the direct contribution limits, the ‘backdoor Roth IRA’ strategy becomes a crucial tool. This method allows high-income earners to indirectly contribute to a Roth IRA.

The process typically involves contributing non-deductible funds to a traditional IRA, and then immediately converting those funds to a Roth IRA. This strategy bypasses the direct income limitations.

While seemingly complex, the backdoor Roth IRA is a legitimate and widely used strategy for Maximizing Your 2026 Roth IRA Contributions when direct eligibility is not met.

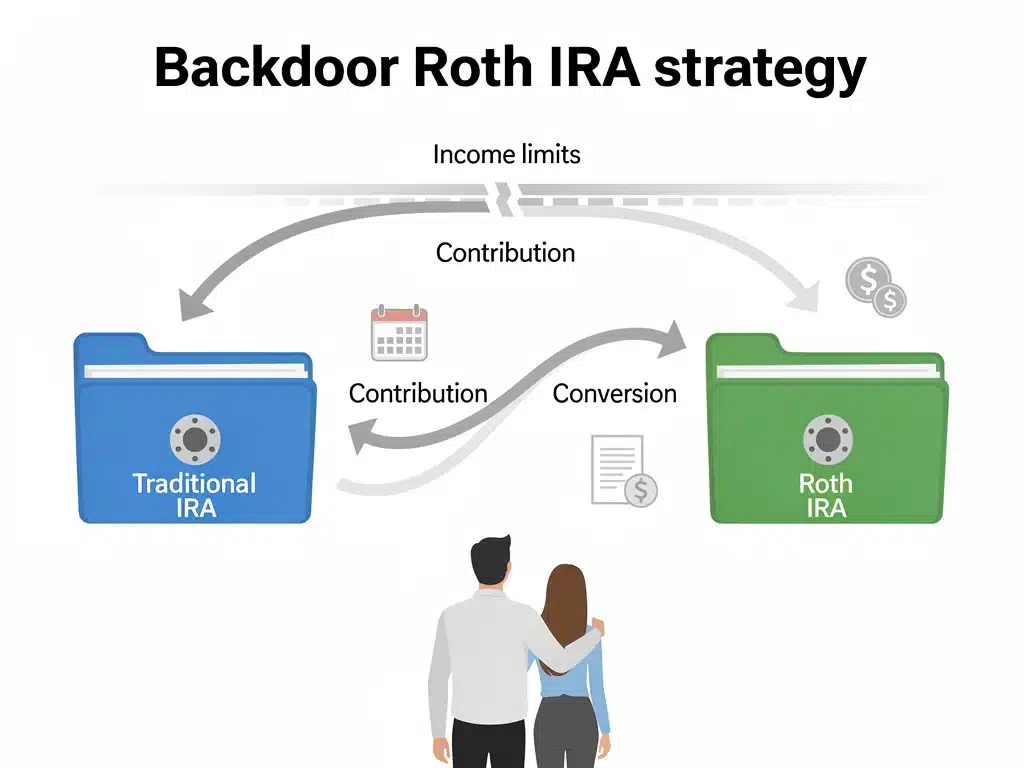

Exploring the Backdoor Roth IRA Strategy

The backdoor Roth IRA strategy is a legitimate method for high-income earners to contribute to a Roth IRA, circumventing the IRS’s direct income limitations. This strategy has gained significant popularity and remains a key tool for retirement planning.

It involves two primary steps: first, making a non-deductible contribution to a traditional IRA, and second, converting that traditional IRA balance into a Roth IRA. This conversion effectively moves funds into the tax-advantaged Roth account.

Understanding the mechanics and potential pitfalls of this strategy is paramount for successful implementation. Proper execution ensures you can still benefit from the tax-free growth offered by a Roth IRA.

Step-by-Step Backdoor Roth Conversion

The first step in a backdoor Roth IRA is to contribute to a traditional IRA. This contribution must be non-deductible, meaning you do not claim a tax deduction for it on your income tax return.

Shortly after, you initiate a conversion of these funds from the traditional IRA to a Roth IRA. The key is to perform this conversion quickly to minimize any potential tax liability on earnings that might accrue in the traditional IRA.

This two-step process effectively allows you to bypass the income restrictions that prevent direct contributions, enabling Maximizing Your 2026 Roth IRA Contributions.

The Pro-Rata Rule and Its Implications

A crucial consideration for the backdoor Roth IRA is the ‘pro-rata rule.’ This rule applies if you hold other pre-tax traditional IRA accounts, such as those rolled over from an old 401(k).

The pro-rata rule mandates that when you convert funds from a traditional IRA to a Roth IRA, the converted amount is treated as partly taxable and partly non-taxable, based on the ratio of your pre-tax IRA assets to your total IRA assets.

To avoid significant tax implications under the pro-rata rule, it is often advisable to have no other pre-tax IRA balances when executing a backdoor Roth conversion. This simplifies the process for Maximizing Your 2026 Roth IRA Contributions.

Optimizing Your Contributions Throughout the Year

While the $7,000 limit applies to the entire calendar year, how you choose to make your contributions can impact your overall financial strategy and investment growth. Spreading contributions throughout the year is often recommended.

Regular contributions, such as monthly or bi-weekly, leverage the principle of dollar-cost averaging. This strategy helps mitigate market volatility by averaging out your purchase price over time, rather than trying to time the market.

This systematic approach not only simplifies the contribution process but also potentially enhances your long-term returns, contributing significantly to Maximizing Your 2026 Roth IRA Contributions.

Dollar-Cost Averaging Benefits

Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. When market prices are low, your fixed contribution buys more shares; when prices are high, it buys fewer.

Over time, this strategy can lead to a lower average cost per share, which can be advantageous for long-term investors. It removes the emotional component of investing, promoting disciplined savings.

This consistent approach is particularly beneficial for retirement accounts like the Roth IRA, ensuring a steady build-up of your portfolio without the stress of market timing.

Maximizing Early Contributions

Contributing early in the year allows your funds more time to grow tax-free within the Roth IRA. Even a few months of additional investment time can make a significant difference over decades.

If you have the financial capacity, making a lump-sum contribution at the beginning of the year can potentially maximize your investment returns. This allows your entire annual contribution to benefit from compounding growth immediately.

However, ensure that such an early contribution does not strain your immediate financial liquidity. Balancing early contributions with your overall financial health is key to Maximizing Your 2026 Roth IRA Contributions.

Considering Other Retirement Savings Vehicles

While Maximizing Your 2026 Roth IRA Contributions is an excellent goal, it’s important to view it within the broader context of your overall retirement strategy. A diversified approach often involves utilizing multiple types of retirement accounts to maximize tax advantages and flexibility.

For many individuals, employer-sponsored plans like a 401(k) or 403(b) form the cornerstone of their retirement savings. These plans often come with employer matching contributions, which are essentially free money and should be prioritized.

Exploring other options such as Health Savings Accounts (HSAs) for those with high-deductible health plans can also provide triple tax advantages, serving as another powerful savings vehicle for future healthcare costs in retirement.

Integrating Roth IRA with 401(k) or 403(b) Plans

If your employer offers a 401(k) or 403(b) plan, especially one with a matching contribution, contributing at least enough to receive the full match should be your first priority. This is a guaranteed return on your investment.

Once you’ve secured the employer match, contributing to your Roth IRA becomes the next logical step, especially if you anticipate being in a higher tax bracket in retirement. The tax-free withdrawals in retirement are a significant advantage.

After Maximizing Your 2026 Roth IRA Contributions, consider increasing your contributions to your employer-sponsored plan, particularly if it offers a Roth 401(k) option, which combines features of both account types.

The Role of Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) offer a unique triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For those with high-deductible health plans, an HSA can be a powerful retirement savings tool.

Many financial experts consider HSAs to be a ‘stealth’ retirement account, as funds can be invested and grown tax-free, similar to a Roth IRA. After age 65, withdrawals for non-medical expenses are taxed as ordinary income, much like a traditional IRA.

Incorporating an HSA into your overall financial plan, alongside Maximizing Your 2026 Roth IRA Contributions, can significantly enhance your retirement security and provide a tax-efficient way to cover healthcare costs.

Monitoring Legislative Changes and Economic Factors

The landscape of retirement planning is not static; it is continually influenced by legislative changes and broader economic factors. Staying informed about potential shifts is crucial for proactive financial management.

Changes in tax laws, adjustments to inflation, and evolving economic conditions can all impact the effectiveness of your retirement strategies. The IRS and Congress regularly review and modify regulations pertaining to retirement accounts.

Financial news outlets, government publications, and reputable financial advisors are excellent resources for tracking these developments. Proactive monitoring ensures your strategy for Maximizing Your 2026 Roth IRA Contributions remains optimized.

Impact of Inflation on Contribution Limits

Contribution limits for retirement accounts, including the Roth IRA, are typically adjusted annually for inflation. This aims to ensure that the purchasing power of your retirement savings is preserved over time.

While the $7,000 limit for 2026 is a projection, it reflects an anticipated adjustment based on inflationary trends. Such adjustments are vital for maintaining the real value of your contributions.

Understanding how inflation impacts these limits helps in long-term financial projections and ensures your strategy for Maximizing Your 2026 Roth IRA Contributions keeps pace with the cost of living.

Potential Legislative Modifications

Congress can introduce legislation that alters the rules surrounding Roth IRAs, including contribution limits, income thresholds, and even the backdoor Roth strategy. While less frequent, such changes can have significant implications.

For instance, there have been discussions in the past about eliminating the backdoor Roth IRA for high-income earners. While not enacted, such proposals underscore the importance of staying vigilant.

Keeping an eye on legislative developments through reliable news sources and financial publications allows you to adapt your strategy for Maximizing Your 2026 Roth IRA Contributions as needed.

Seeking Professional Financial Guidance

Navigating the complexities of retirement planning, especially when aiming for Maximizing Your 2026 Roth IRA Contributions, can be challenging. The rules and regulations are intricate, and personal financial situations vary greatly.

Engaging with a qualified financial advisor can provide personalized insights and ensure your strategies are aligned with your specific financial goals and risk tolerance. An advisor can help you understand income limits, the pro-rata rule, and other nuances.

Their expertise can be invaluable in creating a comprehensive retirement plan that integrates your Roth IRA with other savings vehicles, optimizing your overall financial health.

When to Consult a Financial Advisor

It is advisable to consult a financial advisor if your income approaches or exceeds the Roth IRA direct contribution limits. They can help you determine if a backdoor Roth strategy is appropriate and how to execute it correctly.

If you have multiple retirement accounts, such as traditional IRAs, SEP IRAs, or SIMPLE IRAs, an advisor can help you navigate the complexities of the pro-rata rule. This ensures you avoid unexpected tax liabilities during conversion.

Additionally, an advisor can help you integrate your Roth IRA contributions into a broader financial plan that includes investments, estate planning, and tax optimization, ensuring a holistic approach to Maximizing Your 2026 Roth IRA Contributions.

Benefits of a Comprehensive Financial Plan

A comprehensive financial plan goes beyond simply Maximizing Your 2026 Roth IRA Contributions; it encompasses all aspects of your financial life. This includes budgeting, debt management, investment strategy, and estate planning.

Such a plan provides a clear roadmap to achieving your long-term financial goals, ensuring that each financial decision you make supports your overall objectives. It offers peace of mind and reduces financial stress.

Working with an advisor to develop a personalized plan ensures that your Roth IRA contributions are part of a cohesive strategy, maximizing their impact on your retirement security.

Common Pitfalls to Avoid with Roth IRAs

While Roth IRAs offer significant advantages, there are common mistakes that individuals can make, potentially undermining their benefits. Being aware of these pitfalls is key to ensuring your strategy for Maximizing Your 2026 Roth IRA Contributions is effective and compliant.

One frequent error is exceeding the annual contribution limit without realizing it, which can lead to IRS penalties. Another is failing to understand the income phase-out rules, leading to improper direct contributions.

Additionally, mismanaging the pro-rata rule during a backdoor Roth conversion can result in unexpected tax liabilities. Careful attention to detail and ongoing education are crucial.

Avoiding Over-Contribution Penalties

Contributing more than the annual limit to your Roth IRA can result in a 6% excise tax on the excess amount for each year it remains in the account. This penalty can erode your savings over time.

To avoid this, carefully track all your contributions throughout the year. If you accidentally over-contribute, you must remove the excess contributions plus any earnings attributable to them by the tax filing deadline.

Staying within the $7,000 limit (or $8,000 if aged 50 or older) is a fundamental aspect of Maximizing Your 2026 Roth IRA Contributions without incurring unnecessary penalties.

Understanding the Five-Year Rule

The Roth IRA has a ‘five-year rule’ that dictates when tax-free and penalty-free withdrawals of earnings can begin. There are two distinct five-year periods to consider.

The first five-year period begins on January 1 of the year you make your first Roth IRA contribution. The second five-year period applies to conversions, starting on January 1 of the year the conversion was made.

Failing to understand these rules can lead to unexpected taxes or penalties on withdrawals, impacting the tax-free advantage. Proper planning ensures you comply with these requirements when Maximizing Your 2026 Roth IRA Contributions.

| Key Strategy | Brief Description |

|---|---|

| Hit $7,000 Limit | Maximize annual contributions up to the projected $7,000 for 2026. |

| Backdoor Roth IRA | Strategy for high-income earners to bypass direct contribution limits. |

| Dollar-Cost Averaging | Invest regularly to mitigate market volatility and average purchase cost. |

| Professional Advice | Consult a financial advisor for personalized guidance and planning. |

Frequently Asked Questions About 2026 Roth IRA Contributions

The projected Roth IRA contribution limit for individuals under age 50 in 2026 is $7,000. Individuals aged 50 and older are expected to be eligible for an additional catch-up contribution, further increasing their savings potential for Maximizing Your 2026 Roth IRA Contributions.

Eligibility for direct Roth IRA contributions in 2026 depends on your Modified Adjusted Gross Income (MAGI). The IRS sets specific income thresholds, and if your MAGI exceeds these limits, your ability to contribute directly may be phased out or eliminated. Always verify the latest IRS guidelines.

A backdoor Roth IRA is a strategy for high-income earners to contribute to a Roth IRA when direct contributions are disallowed. It involves making a non-deductible contribution to a traditional IRA, then converting those funds to a Roth IRA. This bypasses income limits for Maximizing Your 2026 Roth IRA Contributions.

Yes, over-contributing to a Roth IRA can result in a 6% excise tax on the excess amount for each year it remains in the account. It is crucial to monitor your contributions and remove any excess amounts plus associated earnings by the tax filing deadline to avoid these penalties.

A financial advisor can provide personalized guidance on Maximizing Your 2026 Roth IRA Contributions, helping you navigate income limits, understand the pro-rata rule for backdoor conversions, and integrate your Roth IRA into a comprehensive retirement plan. Their expertise ensures compliance and optimization.

Perspectives

Maximizing Your 2026 Roth IRA Contributions is more than just hitting a number; it’s about strategically leveraging a powerful tool for your financial future. The projected $7,000 limit offers a significant opportunity for tax-free growth, a benefit that compounds over decades. As economic conditions evolve and legislative discussions continue, staying informed and proactive is essential. The integration of Roth IRAs with other retirement vehicles and the careful consideration of strategies like the backdoor Roth, underpin a robust retirement plan. For those committed to financial security, the steps taken today to optimize these contributions will yield substantial rewards in retirement.

Benefits: A 15% Tax Advantage Guide")